We’re on Android & iOS Also Now!

To use our app, you need to become a member first. Sign up or log in on our website to unlock the full experience.

To use our app, you need to become a member first. Sign up or log in on our website to unlock the full experience.

You’re about six to eight weeks into the semester. The novelty of new classes has worn off. Maybe you’re noticing little leaks in your finances: trips to eat out, impulse buys, textbooks, printing, errands, social outings. If you haven’t revisited your budget since the semester began, now is the time to hit “reset” and tighten up before things spiral.

This October Budget Reset can help you regain control, finish strong, and reduce stress from money worries. Let’s walk through a practical, step‑by‑-step plan.

Reality check: Your actual income and expenses may differ from your initial estimates. If you don’t adjust, you may run out of funds before the term ends.

Behavior correction: Midway is a great moment to spot patterns—overspending, recurring subscriptions, impulse purchases—and correct them.

Stress relief: Money anxiety distracts you from studying, sleeping, social life. A solid budget helps you focus.

Build better habits: Strong financial habits formed in college carry past graduation. According to research, financial education and budgeting behavior are positively linked among college students. Emerald+2DigitalCommons@URI+2

Prevent emergencies: You’ll reduce the chance of scrambling for cash, relying on high‑interest debt, or making bad last‑minute choices.

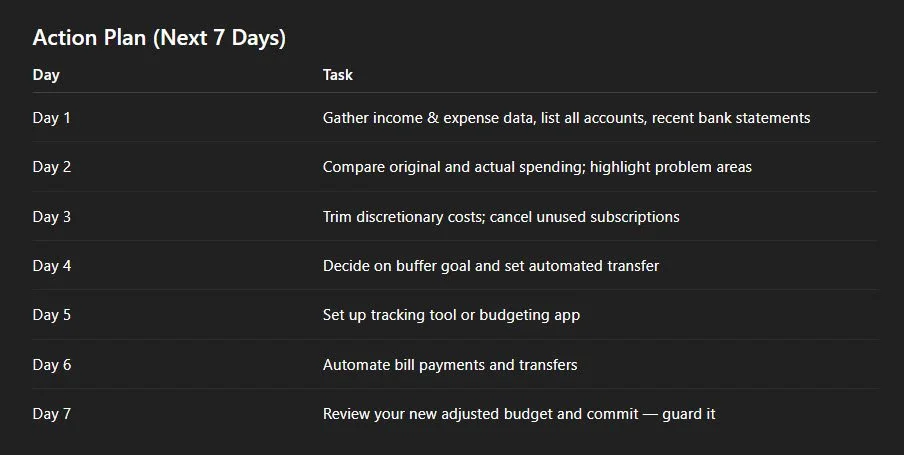

You need to know where you stand. Create a snapshot of your income, expenses, and cash on hand.

What to gather:

All sources of income: part‑time work, work‑study, stipends, parental help, financial aid refunds, scholarship disbursements.

Fixed costs: rent, utilities, phone, transportation, insurance, subscriptions (Spotify, streaming, etc.).

Variable costs: food, groceries, dining out, social, supplies, printing, laundry, personal care.

Unexpected costs: medical, car repair, emergency travel.

Cash in checking/savings, and current credit card or loan balances.

Tip: While estimating, be conservative. Overestimate your expenses, underestimate your income — that way you’re more likely to end with a surplus, not a deficit. sfa.ufl.edu+1

You likely started with a semester or monthly budget. Now let’s compare your original plan to what’s actually happening.

Line by line, compare budgeted vs. actual spending for each category.

Highlight categories where you’re over budget (e.g. dining, entertainment, supplies).

For categories under budget, estimate whether you can maintain or shift that “surplus” into savings or debt repayment.

Adjust your allocations. For example:

If you budgeted $150 monthly for dining out but already spent $180 in October, reduce that allocation going forward.

If you have extra in “miscellaneous,” reassign toward textbooks, an emergency buffer, or paying down credit.

You can’t always do everything. This is where discipline comes in.

Three criteria for trimming:

Need vs. Want: Distinguish what’s essential (food, transportation, shelter, course materials) vs. discretionary (coffee shop runs, streaming upgrades, frequent delivery). sfa.ufl.edu+1

High cost, low value: Which small expenses are adding up? Daily latte? Uber instead of walking? Impulse purchases?

Recurring charges: Review subscriptions and memberships. Cancel what you’re not using.

Examples of cuts:

Cook more at home or in your dorm/kitchen.

Use library resources (reserve textbooks, free printing) instead of buying/renting everywhere.

Carpool, ride a bike, or use public transit instead of solo driving.

Limit impulse buys — wait 24 hours to decide.

Cut or pause unused streaming or app subscriptions.

Even a small buffer can make a big difference when surprises hit (car repair, health expense, extra travel). Aim for $100–$300 initially if you’re tight, then scale upward.

Set up automatic transfers (e.g., $10–$20 per pay period) into a “rainy day” fund. Even a few dollars per paycheck add up. Citizens Bank+1

Discipline is easier when you automate systems.

Use an app or spreadsheet to log every transaction (Wells Fargo’s “My Spending Report,” Mint, or any app you like) wellsfargo.com+1

Automate bill payments (minimums on credit cards, utilities) so no late fees.

Automate transfers to savings or your buffer.

Calendar monthly check-ins (e.g. the 1st of each month) to evaluate and adjust.

Your budget isn’t static. Revisit it monthly (or even weekly) and ask:

Do I need to reallocate funds?

Am I overspending in any category?

Did anything change (new expense, pay raise, extra refund)?

The sooner you detect a leak, the easier to fix it.

One flexible and popular rule is:

50% needs (rent, food, transportation, tuition)

20% savings / buffer / debt paydown

30% wants / discretionary

If income is low, you can adjust to 60/15/25 or 70/10/20, but the structure helps you ensure essentials are covered first. srfs.upenn.edu

You have goals — passing your classes, finishing the semester with momentum, avoiding debt, reducing stress. This isn’t about denying yourself fun altogether, but about staying intentional.

Small daily decisions become habits.

Each dollar you save or redirect gives you more breathing room.

The habits you build now carry you into life after graduation.

As financial literacy research shows, deliberate budgeting behavior is correlated with better financial outcomes among college students. Emerald+1

To support your reset:

Check out our Financial Planning & Budget Tools page (internal link) for worksheets and templates.

Use our FAFSA & Aid Reminders features to ensure you're not missing aid or refund deadlines.

Sign up for our SMS/text reminders so you don’t skip important financial dates.

Visit the Career Simulator / Income Projections to model part‑time work and its net benefit when balancing time and money.

Mid‑semester is not too late — it’s the perfect moment to realign. Be firm with yourself. Be consistent. Be proactive. This reset is not punishment; it’s empowerment. You control your financial choices. Use this reset to finish stronger, reduce stress, and build habits you’ll thank yourself for in future semesters and beyond.

Online now